In the ever-evolving realm of finance, one question looms large: How will the Reserve Bank of Australia (RBA) react to the current inflation slowdown and its potential effects on interest rates? As economic indicators shift, it’s imperative for investors, borrowers, and the broader financial landscape to comprehend the potential ramifications. This article delves into these complexities, offering insights into the possible consequences for mortgage borrowers and the housing market as a whole.

Influence on the Current Mortgage Landscape

Amidst recent lower-than-expected inflation figures, the significance of inflation data in shaping the RBA’s cash rate decisions has waned. While economists often rely on this data for forecasting, the past year has unveiled the inconsistency of a scientific foundation behind the RBA’s actions.

Interestingly, an alternative perspective emerges: achieving the RBA’s inflation target of 2-3% might entail a rise in unemployment. To reach this objective, the RBA could increase interest rates, placing financial strain on businesses and compelling them to reduce their workforce. This approach could promptly lead to higher unemployment rates, affecting a company’s bottom line and cash flow more immediately than alternative cost-cutting methods.

The Road Ahead: More Rate Rises to Come?

Consequently, the horizon hints at more rate increases geared towards elevating unemployment rates. While these forthcoming rate hikes predominantly target businesses’ debt, they could also ripple into consumer home loans. Despite the sluggish pace of inflation, another cash rate increase might be triggered in August to expedite inflation movement. A subsequent move might follow in September or October, with a potential pause during the holiday season.

Borrower Opportunities in Times of Lower Inflation

During periods of diminished inflation, borrowers may not experience substantial advantages in terms of mortgage terms and rates. Banks are likely to maintain their benchmarks for cost of living and household expenditure. However, a silver lining emerges as certain lenders reduce the serviceability buffer for dollar-to-dollar refinances, benefiting “mortgage prisoners” and enabling them to refinance at more competitive interest rates.

Impact on the Housing Market and Affordability

Periods of low inflation often witness heightened housing activity, encompassing property transactions, renovations, upgrades, and investments in furnishings. The desire to enhance living spaces remains robust among Australians. Surprisingly, property prices haven’t significantly decreased, despite the backdrop of interest rate increases. Nevertheless, the aspiration to own homes persists, with new loan enquiries driven largely by prospective buyers aiming to enter the housing market.

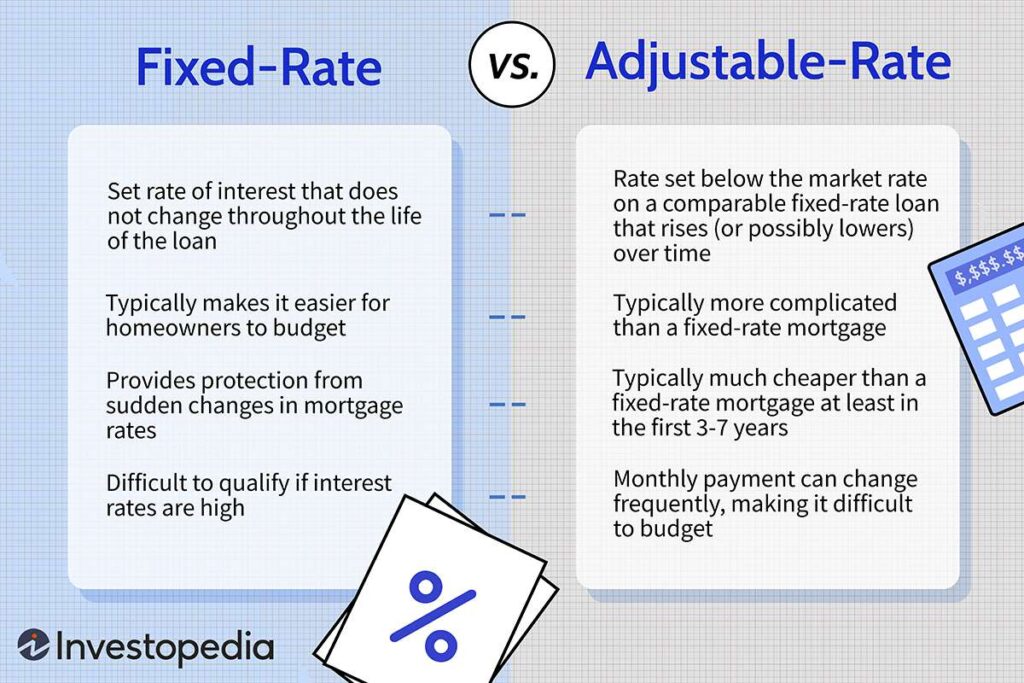

Fixed-Rate vs. Adjustable-Rate Mortgages: A Comprehensive Approach

When advising clients, understanding Australian inflation data is but a fragment of the larger puzzle. Recommendations encompass a broader spectrum, including international factors influencing the Australian economy. Monitoring the actions of the US Federal Reserve and analyzing inflation data from the US provide valuable insights. Presently, despite a decline in inflation, the US Federal Reserve maintains its cash rate, indicating a preference for stable inflation rates before considering rate reductions.

https://www.investopedia.com/mortgage/mortgage-rates/fixed-versus-adjustable-rate/

To comprehend the intricacies of inflation’s impact on the mortgage landscape, a holistic approach is essential. Factors such as RBA decisions, global economic trends, and borrower preferences collaborate to shape recommendations for clients. As we navigate this intricate landscape, a comprehensive perspective ensures well-informed decisions for both the present and the future.

If you’re seeking assistance with navigating the mortgage landscape, understanding inflation’s influence, or making informed borrowing decisions, don’t hesitate to reach out to us. Contact our team for personalised guidance and support tailored to your financial goals. Your journey towards a secure mortgage future starts with a conversation – call us today or visit our website to get in touch.